ETH Is at Its Cheapest Versus Bitcoin Since 2020. Here Is What Institutional Stakers Are Doing.

BASIS Insights, June 18, 2026

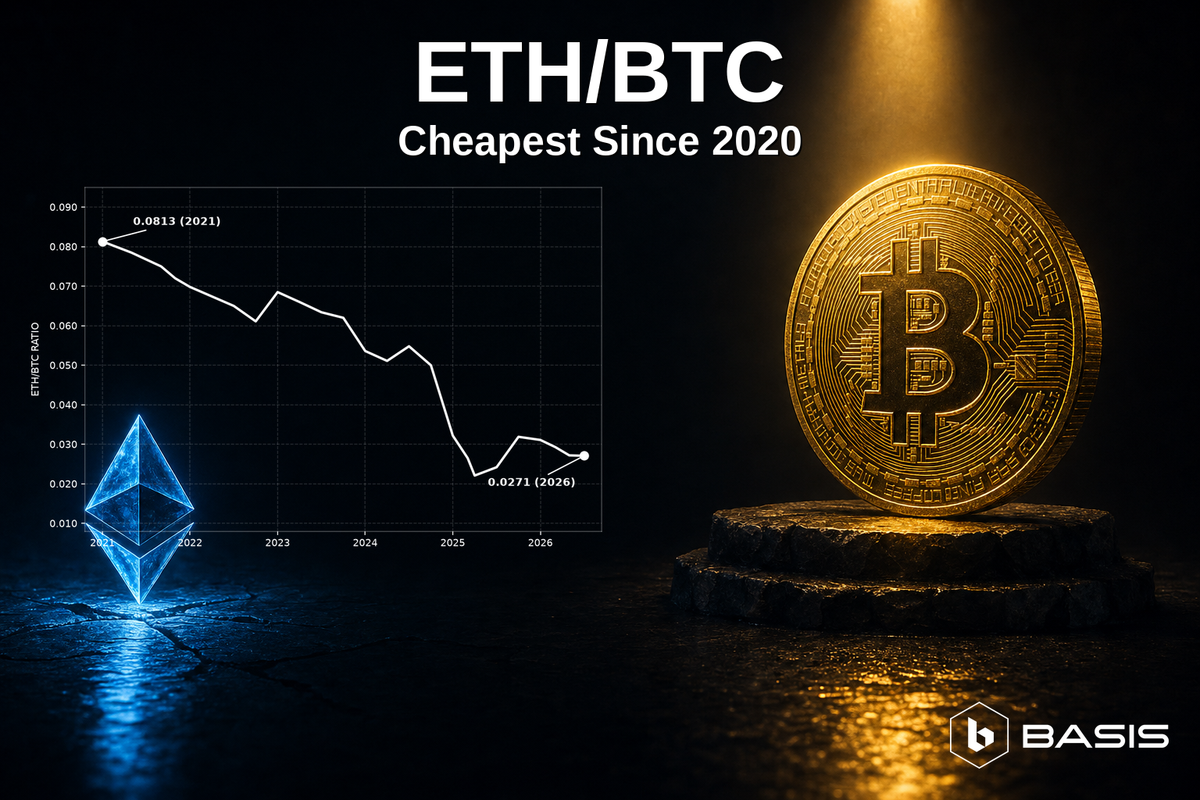

The number is 0.0271.

That is the confirmed ETH/BTC ratio as of June 18, 2026, with ETH at $1,750 and BTC at $64,584. One ETH now buys just 2.71% of one bitcoin. In the confirmed Binance monthly history, ETH/BTC peaked at 0.0813 in November 2021, exactly three times the current ratio.

Strictly, April 2025 printed a lower confirmed monthly ETH/BTC level at 0.0191. That matters. Today is not a fresh cycle low. It is, however, still part of the cheapest ETH/BTC regime of the post-2020 market, and the ratio remains far below the levels that defined the 2021, 2022, and 2023 cycles.

This is the setup institutional stakers are now underwriting: ETH is down 64.6% from its $4,946.05 all-time high, BTC is down 48.8% from its $126,080 all-time high, BTC dominance is 56.2%, and the Crypto Fear & Greed Index is at 15, after 14 consecutive days of Extreme Fear from June 5 through June 18.

The institutional question is not whether ETH has bottomed. It is whether token inventory, staking exposure, and market-neutral yield infrastructure should be managed differently when ETH is historically cheap versus BTC.

The Ratio That Does Not Lie

ETH/BTC removes the dollar denominator. It answers one question directly: is ETH gaining or losing purchasing power against bitcoin?

Right now, the answer is clear. ETH is losing the relative battle.

| Date | Confirmed ETH/BTC | Read-through |

|---|---|---|

| Nov 2021 peak | 0.0813 | Cycle peak, three times today’s ratio |

| Dec 2022 | 0.0723 | ETH still retained most of its relative premium |

| Dec 2023 | 0.0540 | Ratio had weakened, but remained almost double today |

| Apr 2025 | 0.0191 | Confirmed cycle bottom in the supplied Binance history |

| May 2025 | 0.0242 | Initial recovery from the April 2025 bottom |

| Jun 2026 | 0.0271 | Still near multi-year lows |

At 0.0271, ETH/BTC is down 66.7% from the November 2021 peak of 0.0813. It is down 62.5% from December 2022’s 0.0723. It is down 49.8% from December 2023’s 0.0540.

The April 2025 low is the relevant recent precedent. ETH/BTC moved from 0.0191 in April 2025 to 0.0242 in May 2025, a 26.7% relative recovery. By June 2026, the ratio has reached 0.0271, up 41.9% from that April 2025 bottom.

But that recovery has not restored ETH leadership. A move from distressed to less distressed is not the same as a regime reversal. ETH/BTC is still roughly half its December 2023 level and one-third of its November 2021 peak.

That is why allocators should treat the ratio as a state variable, not a trading slogan. ETH is cheap versus BTC, but cheapness can persist. Staking strategy cannot depend on ratio mean reversion arriving on schedule.

Why ETH Is Underperforming

ETH’s underperformance is not explained by one catalyst. It reflects several structural pressures converging at the same time.

First, BTC has the dominant institutional narrative. BTC market cap is $1,292.7 billion, compared with ETH market cap of $211.1 billion. BTC is roughly 6.1 times larger by market capitalization. BTC dominance is 56.2% of a $2.3 trillion total crypto market.

That dominance matters because institutional capital usually enters through the simplest mandate first. The BTC ETF inflow channel reinforces bitcoin as the default institutional crypto beta. Even without relying on unquoted flow totals here, the market result is visible in the data: BTC is down 48.8% from its all-time high, while ETH is down 64.6%.

Second, Ethereum’s fee economics have changed. L2 fee compression improves user affordability, but it also changes how investors value the L1. The prior ETH thesis often linked Ethereum activity directly to L1 fee capture and monetary premium. When more activity is routed through lower-cost execution environments, the simple activity-to-fee-capture narrative becomes less direct. That does not invalidate ETH. It forces investors to reprice the asset with more precision.

Third, supply dynamics are not just about headline issuance. ETH circulating supply is 120.68 million ETH. Binance ETH perpetual open interest is 2,245,800 ETH, which is about 1.9% of circulating supply and roughly $3.93 billion notional at $1,750 ETH. Perpetual markets are therefore large enough to transmit stress into spot pricing. When risk is being reduced, derivatives positioning can matter as much as long-term holder conviction.

Fourth, Solana has fragmented the non-BTC allocation set. SOL is trading at $71.91, down 75.5% from its $293.31 all-time high. That means SOL has not been a clean risk-off shelter. But its presence changes the competitive landscape. ETH no longer owns the smart-contract beta category by default. In periods of capital scarcity, even competing assets that are also down can weaken ETH’s relative bid by splitting attention, liquidity, and mandate design.

Fifth, recent price action confirms the relative pressure. ETH moved from $2,129 on May 20 to $1,583 on June 5, a 25.7% decline, before partially recovering to $1,752 on June 18. BTC moved from $77,552 on May 20 to $61,056 on June 5 and $64,582 on June 18. On a clean May 20 to June 18 point-to-point basis, BTC was down 16.7%, while ETH remained down about 17.7% using the June 18 trajectory price. During the stress leg into June 5, ETH’s drawdown was deeper.

The conclusion is straightforward. ETH is not just down in dollars. It has been repriced lower versus BTC, and the repricing is visible across market cap, dominance, ATH drawdowns, and the ETH/BTC ratio.

What the Fear Data Is Actually Saying

The Crypto Fear & Greed Index is at 15, classified as Extreme Fear. The market has now recorded 14 consecutive days of Extreme Fear from June 5 through June 18.

That is not sentiment decoration. It is liquidity information.

Extreme Fear usually means three things for institutional desks. Liquidity becomes more selective. Leverage is reduced or repriced. Cross-venue dislocations become more important because participants are no longer allocating balance sheet evenly across venues, assets, and instruments.

Spot traders often read Extreme Fear as a contrarian entry signal. That is incomplete. Extreme Fear can precede rebounds, but it can also precede forced deleveraging, lower book depth, and wider execution slippage. The index does not call bottoms. It identifies a market in which risk appetite has collapsed.

Forward-looking stakers watch the same data differently. They are not only asking whether spot ETH rallies tomorrow. They are asking whether token accumulation, hedge design, and neutral execution can continue while the market is impaired.

That distinction matters. A spot trader needs price direction. A token-based allocator can still care about quantity accumulation. A market-neutral infrastructure operator can still care about residual inefficiencies, basis dislocations, funding rate differentials, and execution quality.

Fear changes the opportunity set. It does not remove the need for controls.

The Institutional Calculus

When ETH falls 64.6% from its all-time high and the Lido stETH APY is 2.39%, the arithmetic becomes uncomfortable for dollar-based investors and more interesting for token-based investors.

A staking APY is not a dollar guarantee. It is a token-denominated accrual rate. If ETH is priced lower, the dollar value of each unit of ETH-denominated reward is lower. But the token accumulation rate per ETH remains the same at the quoted APY.

That is the core distinction institutional stakers are focused on.

A USD allocator sees lower mark-to-market value and lower dollar income per ETH. A token-denominated treasury sees the same unit accrual rate on a cheaper asset. If the mandate is to increase ETH inventory over time, lower spot price changes the cost of acquiring the base unit, while the quoted staking rate remains measured in token terms.

This does not make the trade risk-free. It also does not make a 2.39% staking APY a hedge against a 64.6% drawdown from ATH. The yield line item is small relative to the beta move.

That is why the professional question is not “Is staking enough?” It is “What is the asset exposure, what is the yield source, what is the hedge logic, and what controls protect principal when the market is in fear?”

Multi-Asset Neutrality as the Answer

Single-asset staking creates directional exposure. If an allocator stakes ETH, the position still carries ETH beta. The reward is also denominated in ETH. That is useful for token accumulation, but it is not a market-neutral position by itself.

BASIS is designed around a different premise: market-neutral infrastructure should extract value from structural dislocations rather than rely on one asset outperforming another.

BASIS supports BTC, ETH, SOL, and PAXG. Its stTokens are stBTC, stETH, stSOL, and stPAXG, each with a 1:1 quantity peg to the native asset. The strategy is market-neutral and focuses on cross-venue price inefficiencies, basis dislocations, and funding rate differentials.

That matters because current drawdowns are not uniform:

| Asset | Confirmed price | Drawdown from ATH |

|---|---|---|

| BTC | $64,584 | -48.8% |

| ETH | $1,750 | -64.6% |

| SOL | $71.91 | -75.5% |

| PAXG | $4,280 | -23.9% |

A single-asset staking position forces the allocator to accept one asset’s beta profile. A multi-asset neutral stack allows the allocator to separate the asset allocation decision from the yield-infrastructure decision.

The BASIS philosophy is direct: “Alpha is found in the residuals.”

That means the platform is not trying to predict whether ETH outperforms BTC next month. It is designed to capture residual inefficiencies across venues and instruments while operating under deterministic execution, math-constrained decisioning, and state machine risk control.

BASIS is not a passive yield wrapper. It is intelligent yield infrastructure built around capital preservation as an operating principle.

The Booster Mechanics

BASIS publishes a defined booster schedule:

| Holding period | Booster |

|---|---|

| 14D | +10% |

| 30D | +20% |

| 90D | +50% |

| 180D | +100%, or 2x |

This should be understood correctly. The booster schedule is a mechanism for patient capital. It is not a standalone promise of returns and it is not a substitute for the underlying strategy design.

Institutional allocators prefer predictable structures because they reduce operational ambiguity. A defined duration ladder helps investors understand how tenor affects the reward framework before capital is deployed. It also discourages short-horizon behavior during periods of market stress, when reactive liquidity decisions often destroy execution quality.

The fee schedule is also explicit: 0% deposit fee, 0.01% swap fee, and 0.05% withdrawal fee.

In a market where ETH/BTC is near multi-year lows and sentiment is in Extreme Fear, structure matters. A published booster schedule and transparent fee surface allow allocators to model participation mechanics without inventing assumptions.

Infrastructure Credibility

Fear markets expose infrastructure quality.

In a bull run, loose execution can be hidden by rising prices. In a fear market, latency, venue synchronization, hedge timing, and circuit-breaker logic determine whether a strategy captures a residual or inherits directional risk.

BASIS is operated by BASIS DIGITAL INFRASTRUCTURE LTD, a Seychelles IBC with LEI 254900IX2F2KCWNSSS64. BASIS was founded on 2026-02-04 and lists Base58 Labs as Research Partner. According to docs.basis.pro, BASIS holds ISO/IEC 27001:2022, Certificate No. SC62455E, updated March 27, 2026, and ISO/IEC 20000-1:2018. Both certifications are verifiable on IAF CertSearch.

The execution layer is BHLE, with sub-50μs latency and 100K+ OPS. Those numbers matter because market-neutral arbitrage is execution-sensitive. A delayed hedge can convert a basis opportunity into unwanted beta. A stale quote can turn a residual into a loss. High-throughput execution is not cosmetic in this context.

Risk control is equally important. BASIS Sentinel Circuit Breaker, or BSCB, is designed to automatically halt if principal loss risk reaches 0.001%. Defensive Maintenance Mode, or DMM, provides a controlled pause for investigation and stable resumption.

The architecture is state-machine based. That means strategy behavior is constrained by defined system states rather than discretionary improvisation. In Extreme Fear, that distinction matters. Markets move faster, liquidity thins, and the cost of manual ambiguity rises.

Capital preservation is not a slogan here. It is the operating constraint that determines whether market-neutral infrastructure can remain useful when spot markets are hostile.

Conclusion

ETH/BTC at 0.0271 is a fact. An ETH bottom is a forecast.

Institutional stakers should not confuse the two.

ETH is historically cheap versus BTC, but the confirmed Binance history shows that April 2025 was cheaper at 0.0191. The lesson is not to call a bottom. The lesson is to recognize that relative value, token accumulation, and market-neutral yield infrastructure must be managed separately.

The more disciplined institutional response is clear:

This market is not rewarding generic exposure. BTC dominance is 56.2%, ETH is down 64.6% from ATH, and sentiment has been in Extreme Fear for two full weeks.

The institutional takeaway is direct: this is not about calling the ETH bottom. It is about recognizing that market-neutral infrastructure can operate independently of price direction, provided the execution, risk controls, and asset framework are built for that purpose.